Why Millennials Pay Lower For Car Insurance In 2025

Millennials found an easy way to get their premiums as low as possible. Here’s how.

Thousands of young Americans are uncovering hidden car insurance savings in 2025. You can cut your bill by $600 or more in just a few minutes.1

Like many Americans, you’ve probably watched your car insurance premiums go up hundreds of dollars over the past two years.

Even as inflation cooled down, insurance prices stayed high.

But that’s not the case for everyone, especially millennials. And the reason is simple:

Millennials have no shame in shopping for a better car insurance company.

A survey revealed that 42% of millennials compare auto insurance prices yearly, the highest among all age groups.2

They are prepared to vote with their feet if their current company is not competitive enough.

In fact, the Consumer Reports’ 2024 survey of over 40,000 Americans with car insurance revealed that respondents who switched insurers saw a median annual savings of $461.3

Meanwhile, older drivers still think switching companies hurts their rates (it doesn’t). Or that there is some sort of loyalty discount for staying with the same company for years.

But those discounts may never come.

Instead all you get are increased costs for no good reason, because they know you’ll just “eat” the increases.

You may also think it’s a lot of work to find a new company.

And that’s true. With +5,000 car insurance companies in the U.S., finding the best one in your specific state, your specific age, and your specific driving experience can be tough.

Not to mention insurers use complicated pricing formulas that result in prices all over the place and only cause confusion.

These new scoring models—though hidden from the public—are available to regulators. But because they’re so complex, regulators are not able to monitor them deeply.4

The truth is, millennials aren’t making these calculations and reaching out to insurers one by one to see who gives them the best deal.

Instead? They use advanced filtering tools to compare insurance offers and find discounts in a few minutes.

Select Your Age:

Pay less. Stress less. Get more.

© 2025 Coverage.com a Red Ventures Company All Rights Reserved.

This is one of the easiest ways to not only slash your premiums (save $600 or more every year) but also get higher-quality coverage.

It will quickly analyze the October 2025 pricing algorithms of over 70+ carriers and find you discounts based on your specific details.

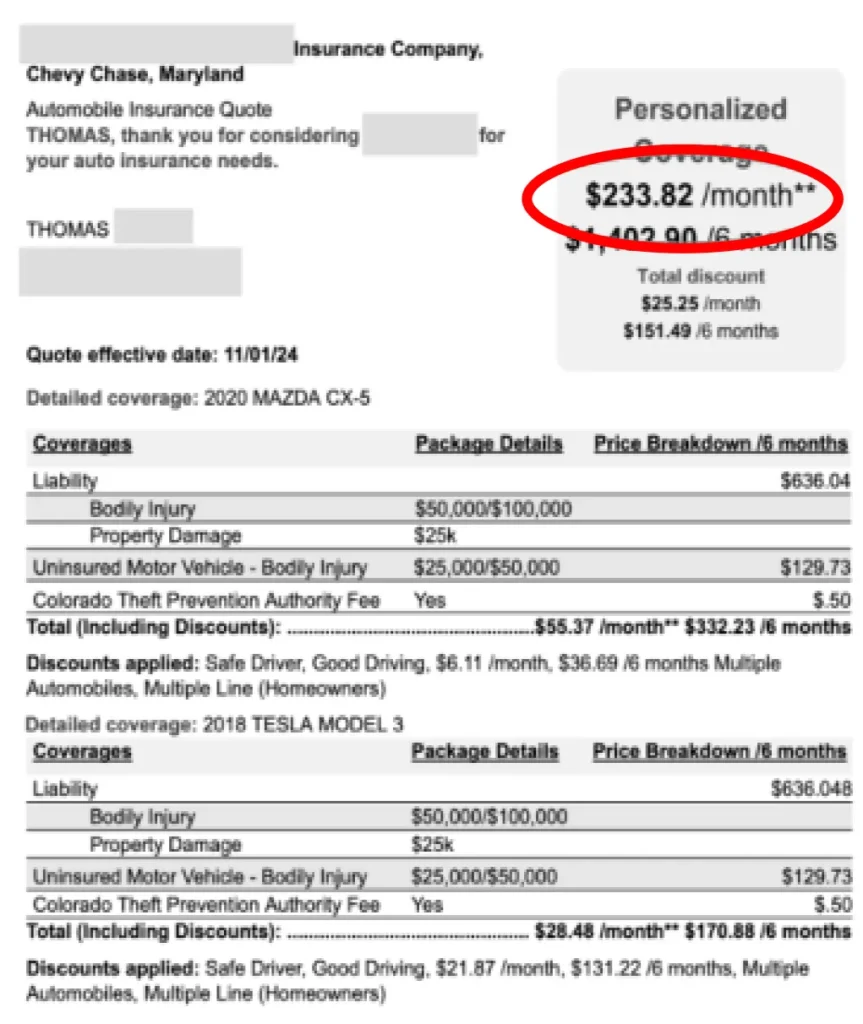

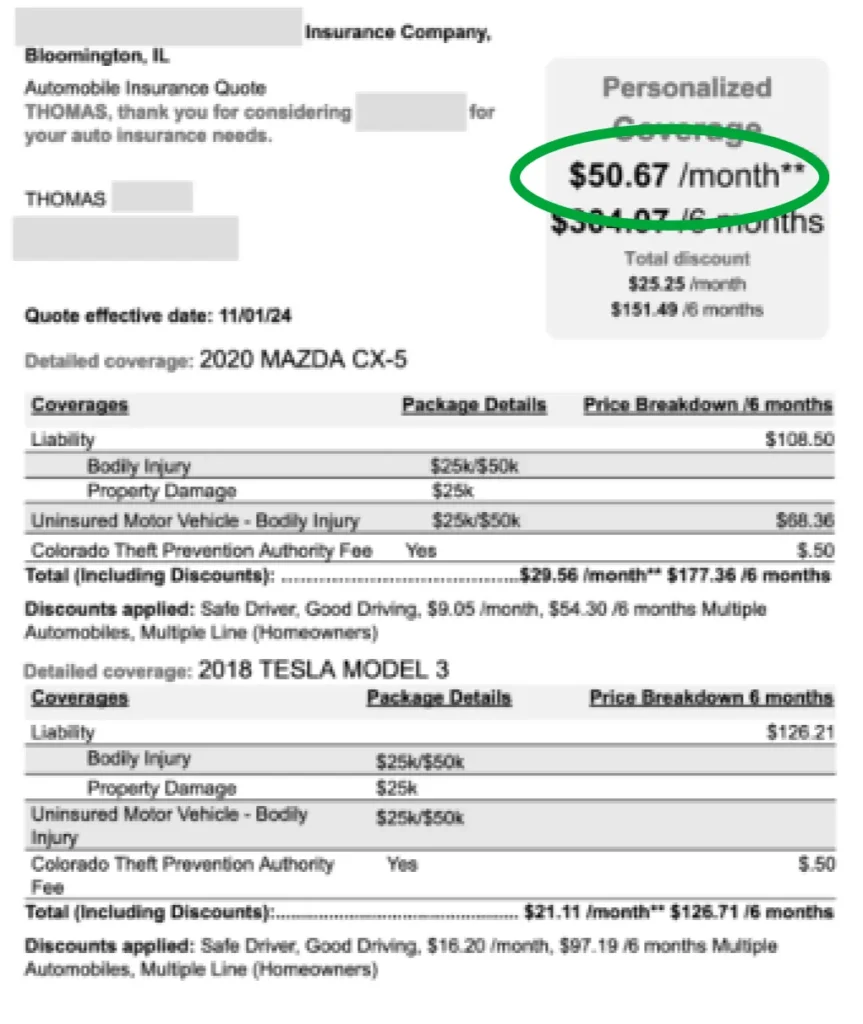

It’s that easy to check if you’re overpaying on car insurance. You no longer need to do hours of heavy research to get savings like this:

*You may get a better or worse quote than the example above depending on your ZIP code, driving record, and car.

You see, thousands of Americans now realize they cannot be dependent on their agent to help them save (agents are paid on commission).

For example, has someone ever told you that if you drive less than 50 miles/day and live in a qualified ZIP code you can get an extremely high discount? And depending on your age you can get an even higher discount.

I’m talking policies as low as $50/month as shown above.

Now you too can take advantage.

Remember: You’re never locked into your current policy. You can cancel mid-year (even if you’ve already paid your bill) and likely be refunded your balance.

Footnotes

- You may get better or worse savings than this depending on your ZIP code, driving record, and car. ↩︎

- https://www.fool.com/money/research/car-insurance-trends-survey/ ↩︎

- https://www.consumerreports.org/money/car-insurance/how-to-lower-your-car-insurance-rates-a9179717041/ (You may get a better or worse quote than this depending on your details.) ↩︎

- https://www.consumerreports.org/cro/car-insurance/auto-insurance-special-report1/index.htm ↩︎